- US bond yields rose to a seven-year high last week, but French bank BNP Paribas says now is a good time to buy bonds.

- Rates strategist Laurence Mutkin argues that markets haven’t correctly priced in a shift in strategy by the US Fed.

- Mutkin says when US stocks fall sharply like they did last week, it’s usually a catalyst for treasury yields to fall.

Markets haven’t priced correctly for a possible change in strategy by the US Federal Reserve, BNP Paribas says.

And the bank’s global head of rates strategy argues it’s time to start buying US 10-year bonds.

Last Wednesday, a selloff in the bond market saw US 10-year bond yields jump to a seven-year high of 3.26%.

The sharp increase sparked a rout of US stocks, which fed into a bloodbath on Asian markets the following day.

When bond yields rise unexpectedly it often leads to higher volatility, because official cash rates are a core part of how markets value other assets such as stocks and corporate bonds.

And recent commentary from the US Fed suggests at least three more rate hikes are still on the cards as the US economy strengthens.

So should investors be wary of the fallout from higher rates? Not just yet, according to Laurence Mutkin, global head of G10 rates strategy at BNP's London office.

"The US 10-year yield is already above our year-end target, and the market is pricing in more than the two further Fed hikes that we expect," Mutkin says.

Mutkin said it's quite common for stocks to fall as rates rise. It makes sense if stock valuations aren't excessive, and the pace of rate hikes matches the pace of economic growth.

Problems arise when yields increase, and all of a sudden stocks look way overvalued and debt levels look excessive.

In that case, the resulting selloff can be so drastic that it creates a negative ripple effect in the real economy.

And in such a scenario, it wouldn't make sense for the Fed to continue hiking rates aggressively.

"It's typical in periods of market stress like the present one, that the rates market should re-price to take account of the possibility that the Fed's policy path will have to change," Mutkin says.

However, "that has not yet happened".

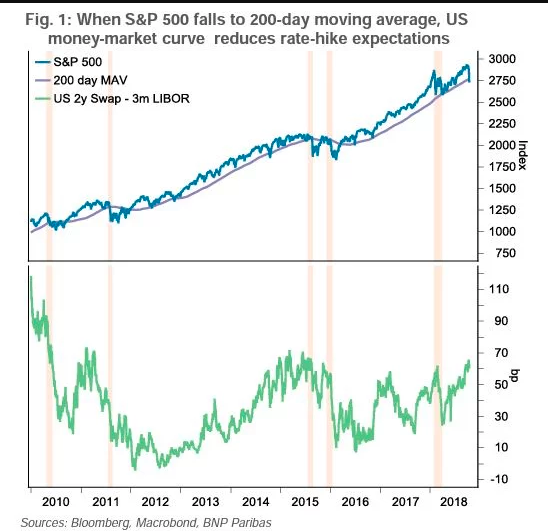

For evidence, Mutkin pointed to the S&P500, which fell below its 200-day moving average last week.

Historically, markets have usually reduced their rate-hike expectations when that happens:

"With the recent S&P fall, and not much reaction from the 2-year note, there is a significant probability of a treasury rally in our view," Mutkin says.

When last week's stock selloff gathered steam, US 10-year yields fell from 3.26% to 3.14% as capital moved back into safe-haven assets. But they crept higher on Friday to close the week at 3.17%.

However, Mutkin said other factors will help drive demand for US bonds, starting with the debt crisis in Italy.

He also sas US data is starting to soften, highlighting the latest CPI data which showed annual inflation growth slowed in September.

BNP's "favored positioning in this context is for trades which protect against risk aversion".

Mutkin's view highlights the tricky balancing act faced by the Fed as it tightens monetary policy: try to avoid the economy overheating, but don't let growth fall off a cliff.

The next update on Fed policy will be the minutes from the bank's September meeting, scheduled for release on Wednesday night.